Market developments:

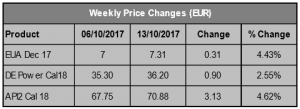

- Carbon gains 4% to end the week at €7.31

- Intra-week gains fuelled by hope of Phase IV reform and ‘Brexit clause’

- Clean dark spreads fall as coal and carbon price gains outstrip power

- ‘Brexit clause’ (Amendment 47) advances with minimal changes

- Trilogue fails to find agreement on Phase IV reforms

- Redshaw Advisors are hiring. Check it out and share our link.

EU Allowance Auction Overview:

- Auction volume this week falls slightly to ~21.5Mt (vs ~22.1Mt)

- Auction supply will remain high in October as ~91.5Mt comes to market, slightly down on September’s ~91.8Mt

- See auction table below for details

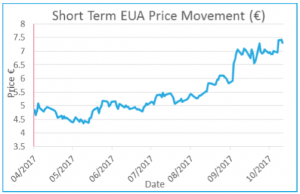

EUA PRICE ACTION

Carbon moved 31c higher last week despite falls in the clean dark spreads and EU politicians failing to find agreement on the Phase IV EU ETS reforms. The gains came ahead of the trilogue meeting on Thursday and perhaps more importantly ahead of the Aviation reform meeting that was also scheduled to discuss Amendment 47 (the ‘Brexit clause’). With the main price driving reform, the rate of withdrawal of EUAs into the MSR, already agreed for Phase IV the ‘Brexit clause’ is the new kid on the block likely to have a market impact. The support for Amendment 47 with only minor changes from Member States makes it almost certain that it will pass int

Carbon moved 31c higher last week despite falls in the clean dark spreads and EU politicians failing to find agreement on the Phase IV EU ETS reforms. The gains came ahead of the trilogue meeting on Thursday and perhaps more importantly ahead of the Aviation reform meeting that was also scheduled to discuss Amendment 47 (the ‘Brexit clause’). With the main price driving reform, the rate of withdrawal of EUAs into the MSR, already agreed for Phase IV the ‘Brexit clause’ is the new kid on the block likely to have a market impact. The support for Amendment 47 with only minor changes from Member States makes it almost certain that it will pass int o law and render UK issued allowances from 1st January, 2018 invalid for compliance (see ‘Other news’ for more information). Following marathon trilogue talks (also see ‘Other News’) the deadlock on the final element of the Phase IV reform package continued and carbon opened lower on Friday morning. However, prices managed to claw back much of the losses through the rest of Friday demonstrating that last week’s EUA strength was not down to speculators anticipating a positive result. Relatively strong auction results also demonstrate that underlying demand is strong. And due to the current mixture of bullish factors traders are unlikely to help the market go down by running short positions for fear of further developments that have caused sharp price rises in recent weeks. Price Impact: that carbon can hold on to most of its gains last week despite weaker clean dark spreads and a failed trilogue tells us that underlying demand is strong for other reasons and means that continued gains cannot be ruled out.

o law and render UK issued allowances from 1st January, 2018 invalid for compliance (see ‘Other news’ for more information). Following marathon trilogue talks (also see ‘Other News’) the deadlock on the final element of the Phase IV reform package continued and carbon opened lower on Friday morning. However, prices managed to claw back much of the losses through the rest of Friday demonstrating that last week’s EUA strength was not down to speculators anticipating a positive result. Relatively strong auction results also demonstrate that underlying demand is strong. And due to the current mixture of bullish factors traders are unlikely to help the market go down by running short positions for fear of further developments that have caused sharp price rises in recent weeks. Price Impact: that carbon can hold on to most of its gains last week despite weaker clean dark spreads and a failed trilogue tells us that underlying demand is strong for other reasons and means that continued gains cannot be ruled out.

WEEK AHEAD

All eyes will be on Wednesday’s aviation reform meeting which is crucial because it features further discussion of Amendment 47. Without further changes to the text, which seem unlikely considering the overwhelming support for the amendment, the EUA market risks being split in two and EUA prices look likely to move higher. However, it will be a race against time to ensure it is passed into law before the end of the year. The UK could respond at any time. Last week carbon appeared to be immune to clean dark spread falls but if coal continues to set new highs it will eventually affect carbon prices. However, with such a mixture of bullish price drivers more may have to fall away for the impact to be felt.

OTHER NEWS

UK’s alternative to Amendment 47 brushed aside leaving the potential for an EUA market split

An alternative text to Amendment 47 (the Brexit clause) supplied by the UK, that would have solved the market impact described in our previous weeklies, has been shown little regard by EU Member States who overwhelmingly voted in support of the original text with a few minor amendments. The alternative text was tabled by the UK in response to EU politicians’ attempts to void all UK issued allowances from 1st January 2018 and although not perfect, it worked. As the amendment stands it is highly likely to increase the costs for all EU installations in the EU ETS except UK installations which is surely not the intended outcome of an amendment increasingly looking like it was designed to put pressure on Brexit negotiations.

With a viable alternative on the table and the risks becoming clearer, the support for the amendment from EU politicians is baffling.

Phase IV reform agreement eludes politicians

Thursday’s trilogue meeting failed to find a compromise on the Phase IV reform package despite a push until around 3 a.m. in a marathon session. Nearly all elements of the reform are agreed, however, one final sticking point on the use of Modernisation Fund money for coal fired power stations continues to divide the Member States and the EU parliament. The Member States support the use of funds for coal fired power projects, however, the EU parliament are staunchly against it. Disagreements over the auction flexibility share to avoid the Cross Sectoral Correction Factor were resolved as Member States gave up a further 0.5% from the auction share and added 100Mt into the Innovation Fund, in place of allowances that can now be used for free allocation. At least one more trilogue will need to be scheduled for agreement to be found, it is reported the next meeting will take place on 8th November, 2017.

Clean Growth Strategy re-affirms UK commitment to carbon pricing

The UK set out its ‘Clean Growth Strategy’ last week that re-affirmed, and set out how the UK intends to achieve, its emissions reduction commitments. It also re-affirmed the UK’s commitment to using carbon pricing in its emission reduction efforts. Although continued EU ETS participation is uncertain the UK government said “Leaving the EU will not affect our statutory commitments under our own domestic Climate Change Act and indeed our domestic binding emissions reduction targets are more ambitious than those set by EU legislation”. Noteworthy for current UK based installations is the commitment to carbon pricing, “we remain firmly committed to carbon pricing as an emissions reduction tool whilst ensuring energy and trade intensive businesses are appropriately protected from any detrimental impacts on competitiveness.” Therefore, some form of UK ETS appears to be the front runner to replace the EU ETS should the UK leave it.